Corporate Tax Reform has emerged as a pivotal issue in the ongoing tax policy debate, especially as Congress prepares for a potential tax overhaul in 2025. With key provisions of the 2017 Tax Cuts and Jobs Act on the verge of expiration, both corporate tax rates and the future of the Child Tax Credit are under scrutiny. Experts have mixed views on the economic impact of tax reform, particularly regarding how the changes initiated by the TCJA have affected business investments and wages. Recent analyses challenge the notion that cutting corporate taxes automatically stimulates growth, highlighting instead that the real-world outcomes have been more nuanced. As lawmakers grapple with these pressing issues, the implications of corporate tax reform are set to shape discussions in the lead-up to the next election.

The ongoing discussions surrounding corporate fiscal policy and tax rates are increasingly gaining traction as America braces for significant changes in tax legislation. As the 2017 Tax Cuts and Jobs Act faces expiration, crucial aspects like the corporate tax structure and family-focused relief measures, such as the expanded Child Tax Credit, are pivotal talking points in today’s political landscape. Stakeholders from various sectors are assessing the benefits and drawbacks of the tax adjustments implemented in recent years, focusing on their effects on employment and corporate investment behaviors. Many economists and political analysts are weighing in on how these legislative changes have influenced overall economic conditions, prompting a deeper examination of tax policies aimed at stimulating business growth. With the election year approaching, the conversation around corporate tax reform will undoubtedly remain a central theme in the fight for voters’ support.

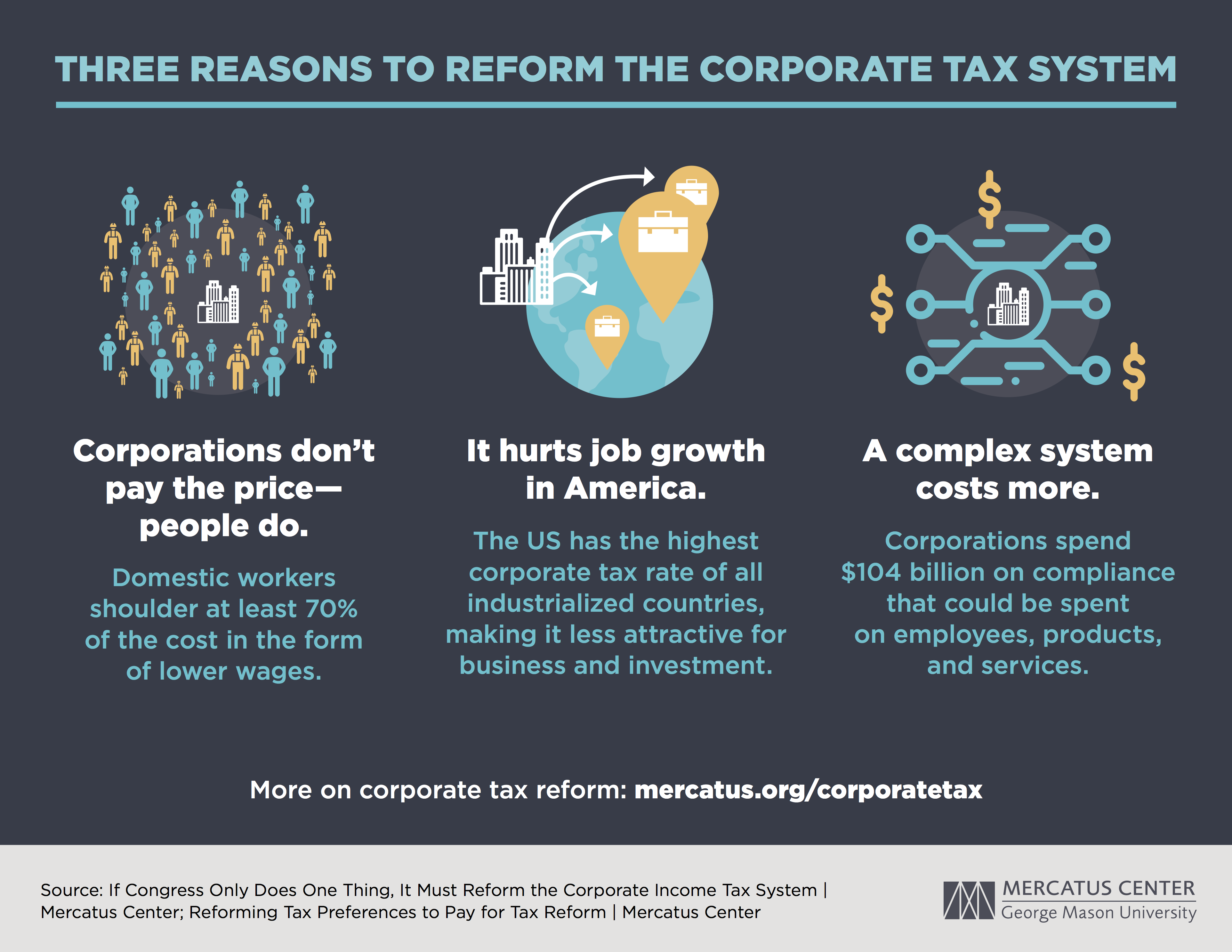

The Urgency of Corporate Tax Reform

As Congress moves toward the 2025 tax battle, the discussion around corporate tax reform is becoming increasingly urgent. The expiration of key provisions from the 2017 Tax Cuts and Jobs Act (TCJA) has reignited debates on whether corporate tax rates should be raised or cut further. Many lawmakers and economists point to the TCJA as a critical moment for changing how corporate taxation is handled in the U.S., reflecting both the need for reform and the evolving landscape of the global economy. Given the substantial revenue lost through corporate tax cuts—estimated at $100 billion to $150 billion annually—many believe that a reassessment is necessary to ensure financial stability in the face of looming budget shortfalls. The tension between maintaining low corporate tax rates to promote growth and the reality of declining federal revenue is a core part of this ongoing discussion.

The realities of economic change at play underscore the importance of corporate tax reform. As the study conducted by Gabriel Chodorow-Reich and his co-authors highlights, merely cutting rates does not guarantee increased investment or wage growth—a claim frequently made by advocates of lower taxes. Instead, reform may need to come in the form of reinstating provisions that encourage immediate capital expensing, which could drive actual growth better than perpetually low tax rates. In essence, corporate tax policies must reflect the modern economic landscape, characterized by increased globalization and competition, to effectively stimulate real investments and job creation.

Frequently Asked Questions

What are the main aspects of Corporate Tax Reform under the Tax Cuts and Jobs Act?

The Tax Cuts and Jobs Act (TCJA) of 2017 significantly reformed corporate tax rates by reducing the federal statutory rate from 35% to 21%. Key aspects included immediate expensing provisions for capital investments, changes to international taxation, and a temporary expansion of the Child Tax Credit. These reforms aimed to incentivize business investment and spur economic growth.

How did the Tax Cuts and Jobs Act impact corporate tax revenue?

Following the implementation of the Tax Cuts and Jobs Act, corporate tax revenue initially dropped by nearly 40%. However, revenue began to rebound starting in 2020 as business profits exceeded expectations, driven by factors such as supply chain shifts and increased domestic profit reporting by U.S. multinationals. Overall, while the TCJA’s cuts reduced immediate revenue, they also set the stage for stronger profits and revenue recovery in subsequent years.

What has been the economic impact of the Corporate Tax Reform introduced by the TCJA?

According to analysis by economists, the economic impact of the Tax Cuts and Jobs Act included an approximate 11% increase in capital investments by firms. While there were modest wage increases observed, the long-term effects on economic growth and investment levels indicate that firms respond positively to corporate tax policy changes, especially through targeted incentives like expensing.

Is there a debate on whether to raise corporate tax rates after the TCJA?

Yes, there is an ongoing debate regarding the potential to raise corporate tax rates to fund new initiatives and support the expiration of provisions targeted at households. Politicians are divided, with some advocating for higher rates to enhance government revenue and invest in social programs, while others argue for maintaining or further reducing rates to stimulate economic growth.

How has the Child Tax Credit been affected by Corporate Tax Reform discussions?

The expansion of the Child Tax Credit, which was included in the Tax Cuts and Jobs Act, is set to expire at the end of 2025. This has become a key talking point in the tax reform debate, with proponents arguing for its renewal to support families, while opponents believe that raising corporate rates could help finance such benefits without exacerbating the budget deficit.

| Key Point | Details |

|---|---|

| Tax Rates Debate | Congress is facing discussions on raising or cutting corporate tax rates as they approach the expiration of parts of the TCJA. |

| 2017 Tax Cuts and Jobs Act | The TCJA reduced the corporate tax rate from 35% to 21%, aiming to spur growth but significantly impacting federal revenue. |

| Corporate Tax Revenue Impact | Following the TCJA, corporate tax revenue initially dropped but began to recover from 2020, exceeding forecasts due to surging profits. |

| Economic Effects of TCJA | The law led to slight increases in wages and business investments, with only modest benefits offsetting revenue losses. |

| Future Tax Policy Challenges | With the expiration of key provisions, the upcoming tax policy discussions will need to address the balance of corporate tax reforms. |

Summary

Corporate Tax Reform is at the forefront of Congressional discussions as they approach significant legislation changes ahead of 2025. The 2017 Tax Cuts and Jobs Act has sparked a contentious debate regarding the effectiveness of corporate tax cuts and revenue implications. Recent studies, especially by Gabriel Chodorow-Reich and his colleagues, provide valuable insights into how these reforms have affected investments, wages, and overall tax revenue. With upcoming provisions set to expire, lawmakers face critical decisions about the future direction of corporate taxation, seeking a balance that promotes economic growth while maintaining federal revenue.