The commercial real estate crisis is becoming an escalating concern as high office vacancy rates plague major urban centers, raising questions about the broader economic implications. As businesses adapt to new work models, many office buildings sit empty, leading to significant declines in property values, especially in cities like Boston where vacancy rates soar between 12% and 23%. Coupled with looming deadlines for a wave of real estate loans coming due by 2025, the stability of the banking sector may face a serious threat if delinquencies rise amid an economic downturn. Banking experts warn that these dynamics, combined with fluctuating interest rates, could create a potentially volatile financial environment. Stakeholders are wary, fearing the cascading impacts on both commercial real estate investments and the wider economy as they brace for the unfolding effects of this crisis.

As we witness increasing challenges in the property market, the term “commercial property predicament” aptly captures the concerns surrounding the ongoing instability in real estate investments. The surge in office vacancy rates, primarily driven by shifts in workplace dynamics post-pandemic, has left landlords and lenders grappling with diminished asset values. With a considerable amount of commercial property loans maturing soon, the banking sector may face significant ramifications if these debts are not managed effectively. Experts in finance and real estate are emphasizing the potential consequences of this situation, as they scrutinize interest rates and their relationship with overall economic health. It is imperative to understand these interconnected variables as the repercussions of the commercial real estate crisis unfold.

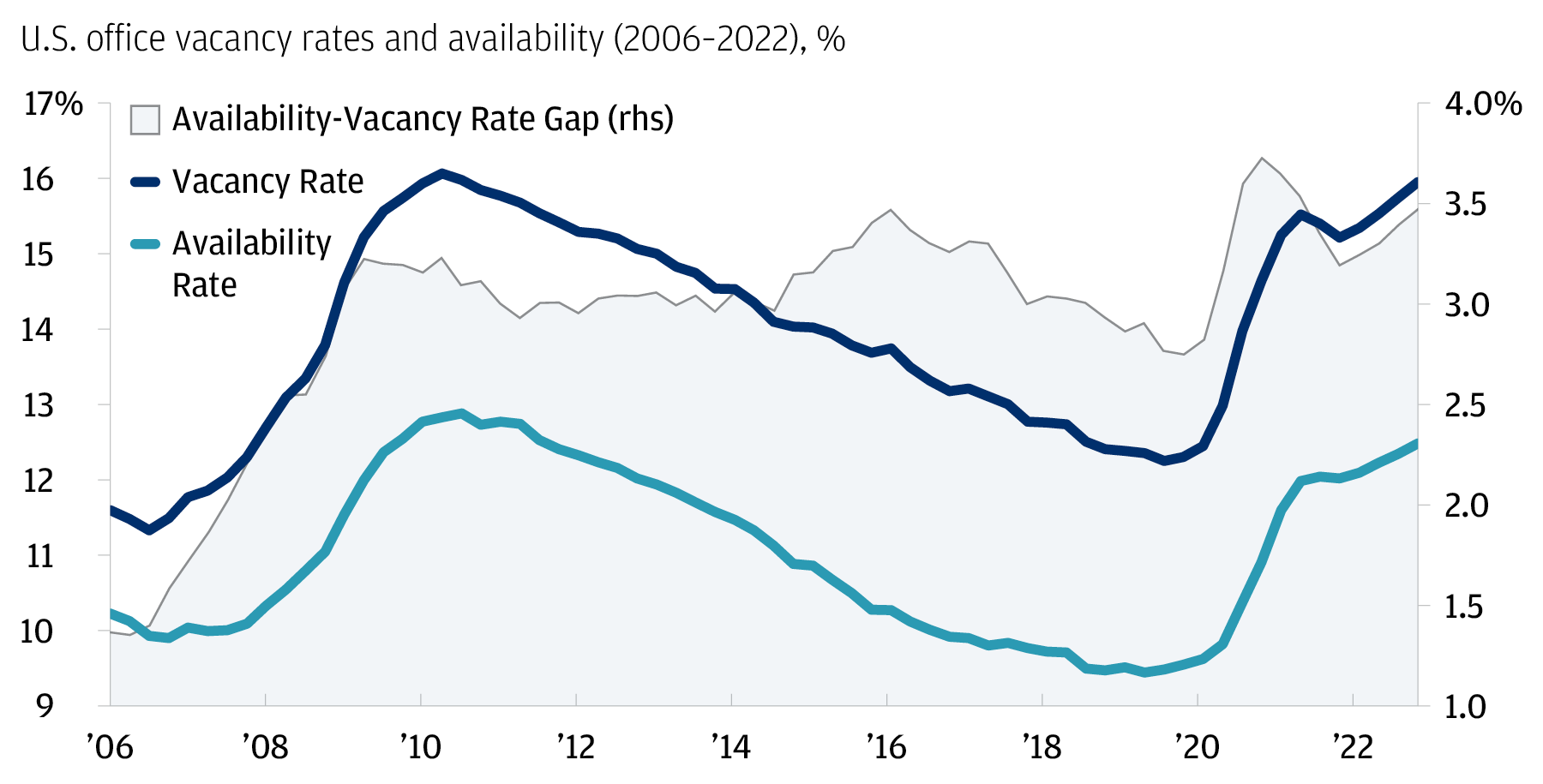

Impact of High Office Vacancy Rates on the Economy

High office vacancy rates pose a substantial risk to the broader economy, especially in major urban areas. As businesses have adapted to changing work environments post-pandemic, the demand for office space has declined significantly, leading to vacancies that range from 12% to 23%. This surge in office vacancies erodes property values and curtails investments in commercial real estate, which directly affects employment and per capita income in metropolitan regions. Furthermore, the continued presence of vacant office buildings can lead to a decline in local businesses that depend on foot traffic, creating a detrimental cycle for local economies.

Moreover, the rising office vacancy rates correlate with increased concern for the financial health of banks heavily invested in commercial real estate loans. With a significant portion of these loans reaching maturity, a high vacancy rate could lead to rising delinquency rates among borrowers. If banks begin to see severe defaults, it can result in stricter lending policies that will further constrain capital flow into the economy, thereby slowing economic recovery. Experts warn that without mechanisms to manage these vacancies and support affected sectors, we could witness a domino effect that impacts various facets of the economy.

The Looming Commercial Real Estate Crisis

The commercial real estate sector is on the brink of a crisis due to a combination of rising interest rates and high vacancy rates. As property values diminish, many commercial real estate loans come due this year, with over 20% of $4.7 trillion in mortgage debt requiring repayment. The challenge is particularly daunting for smaller banks that are less regulated and more vulnerable to economic shocks caused by a surge in delinquencies. This looming crisis could lead to a wave of bankruptcies among firms, creating additional pressure on regional banks and impacting the banking sector as a whole.

Many market experts, including economists like Kenneth Rogoff, have indicated that while the losses may cause significant discomfort within the banking sector and lead to some regional failures, they do not foresee a catastrophe akin to the 2008 financial crisis. They emphasize that stringent post-crisis lending regulations have equipped larger banks to withstand the impacts of commercial real estate failures better. However, as the economic downturn unfolds, the long-term consequences of this crisis could unravel, especially if interest rates do not decrease, creating a precarious environment for simultaneous economic growth.

Effects of Interest Rates on Real Estate Loans

Interest rates have a direct and profound effect on the landscape of real estate loans, influencing both the cost of borrowing and the demand for properties. Over the past few years, low interest rates led many investors to over-leverage themselves, believing that rates would remain low indefinitely. However, as the Federal Reserve maintains a cautious approach to rate cuts, commercial real estate investors face increased borrowing costs that complicate their financial landscapes. Those unable to refinance their loans as they mature may find themselves in precarious financial situations, exacerbating the existing high office vacancy dilemma.

Additionally, high-interest rates create a ripple effect throughout the economy, influencing consumer spending and business investments. Small and regional banks that had generously lent during periods of low rates may struggle as increasing costs and uncertainty deter broader economic activity. Higher interest payments can squeeze businesses, leading to tighter budgets and reduced investments, which can ultimately stifle economic growth and recovery. Stakeholders across various sectors must navigate this challenging environment, understanding that fluctuating interest rates not only affect the housing market but also reverberate through the entire economy.

Banking Sector Impact of Commercial Real Estate Debt

The potential for a crisis in the commercial real estate sector has raised alarms about the stability of the banking sector, particularly for smaller and regional banks. These institutions often have higher concentrations of commercial real estate loans that face maturity, making them susceptible to losses if borrowers default due to rising vacancy rates and declining property values. The linkage between commercial real estate performance and bank health is critical, as failures in this area can influence credit availability for consumers and small businesses, curtailing overall economic activity.

However, major banking institutions, including the six largest U.S. banks, are likely better positioned to withstand potential shocks from the commercial real estate sector. Their diversified portfolios, combined with the financial safeguards established since the 2008 crisis, provide a buffer against localized failures. Nonetheless, if a pattern of delinquencies emerges, it could still hinder regional economic stability and lead to more stringent lending conditions, which would ultimately affect consumers and businesses reliant on easy access to credit.

Strategies to Mitigate Commercial Real Estate Crisis

Addressing the looming commercial real estate crisis requires strategic planning and intervention to stabilize the affected sectors. Policymakers could consider implementing targeted relief measures, such as tax incentives for property owners who convert vacant office spaces into residential units. This approach could alleviate some of the pressure caused by high office vacancy rates while also addressing the housing shortage in urban areas. Moreover, innovative financing solutions such as loan forgiveness or extended repayment terms could provide relief for borrowers struggling to meet obligations during tough economic conditions.

Additionally, collaborative efforts between public and private sectors could foster new opportunities for redevelopment in areas impacted by this crisis. By leveraging federal support and encouraging partnerships with private investors, stakeholders can explore creative ways to repurpose underutilized commercial properties, generate jobs, and stimulate local economies. However, timely action is crucial; without concerted efforts to tackle the challenges posed by the commercial real estate declining demand, a more profound economic downturn could be on the horizon.

Long-term Predictions for Commercial Real Estate

Looking ahead, some market analysts predict a significant transformation in the commercial real estate landscape. The shift towards remote and hybrid work may permanently alter the demand for traditional office spaces, prompting a reevaluation of real estate valuations and investment strategies. Investors may need to adapt by focusing on properties that cater to evolving work preferences, such as flexible workspace solutions or hybrid office environments that accommodate both in-person and remote workers. Such adaptations could redefine the future of commercial real estate, shifting from the conventional models that dominated prior to the pandemic.

In this evolving context, it will be essential for investors to remain vigilant and responsive to market trends while managing their risk exposure amid rising interest rates and potential economic headwinds. The key to navigating these changes will rest on enhancing financial resilience and adopting innovative approaches to real estate development and investment. Long-term sustainability in the commercial real estate sector may involve a pivot towards environmentally sustainable practices and technologies that appeal to both tenants and investors, enhancing property value even amidst challenging economic conditions.

Consumer Impact of Commercial Real Estate Failures

Beyond the immediate financial repercussions for banks and investors, the commercial real estate crisis has broader implications for consumers. High vacancy rates and the potential failure of businesses tied to commercial spaces could lead to job losses, reduced income, and heightened economic uncertainty for many households. Consumers might face stricter lending conditions as banks navigate increased risk exposure, making it more challenging to finance major purchases such as homes or vehicles. This confluence of factors could slow consumer spending, significantly hampering overall economic recovery.

Moreover, if pension funds heavily invested in commercial real estate see substantial losses, retirees and employees depending on those funds might experience diminished returns. The cascading effects of a declining commercial real estate market could magnify existing disparities, particularly for those already facing economic challenges. To mitigate these effects, proactive measures by local governments, financial institutions, and community organizations will be essential in supporting consumers and maintaining economic stability during tenuous times.

Preparing for Future Economic Downturns

As we observe the current vulnerabilities within the commercial real estate sector, it is imperative for stakeholders to prepare for potential economic downturns. Resiliency strategies must include diversification of investment portfolios and the establishment of contingency plans for various economic scenarios. By anticipating shifts in consumer behavior and market demands, investors can better position themselves to weather storms and capitalize on emerging opportunities amid uncertainty. This way, even if the commercial real estate sector faces future crises, the overall economic stability may be preserved.

Additionally, fostering a collaborative relationship between financial institutions, policymakers, and businesses is crucial for creating a supportive framework that can respond efficiently to market fluctuations. Maintaining open communication channels and sharing resources effectively can enhance the adaptability of various sectors, ultimately steering financial systems away from the brink of crisis. Simplifying regulatory processes to facilitate the movement of capital during turbulent times is crucial to ensure that economic shocks in the commercial real estate sector do not translate into a full-blown recession across the broader economy.

Frequently Asked Questions

What are the implications of high office vacancy rates on the commercial real estate crisis?

High office vacancy rates are a significant contributor to the current commercial real estate crisis, particularly in major U.S. cities where these rates range from 12% to 23%. These elevated vacancy levels lead to decreased property values, which in turn can threaten the stability of financial institutions heavily invested in real estate loans. As businesses adapt to new work environments post-pandemic, the demand for office space may remain suppressed, posing ongoing challenges for investors and impacting the broader economy.

How will rising interest rates affect the commercial real estate crisis?

Rising interest rates play a pivotal role in exacerbating the commercial real estate crisis. Since many investors over-leveraged their assets during periods of low interest, the increase in borrowing costs is now causing significant financial strain. This not only impacts the ability to refinance existing real estate loans but also lowers the attractiveness of commercial real estate projects. Consequently, as the cost of borrowing increases, the risk of defaults on these loans rises, intensifying the crisis in the sector.

Could an economic downturn worsen the commercial real estate crisis?

Yes, an economic downturn could significantly worsen the commercial real estate crisis. As economic activity slows, businesses may cut back on commercial space needs, further increasing office vacancy rates and depressing property values. An economic downturn could also lead to higher delinquency rates on commercial real estate loans, affecting the banking sector and potentially prompting a wider financial crisis if substantial losses are incurred by banks with heavy investments in real estate.

What is the potential impact of the commercial real estate crisis on the banking sector?

The commercial real estate crisis poses a potential risk to the banking sector, particularly for regional banks that hold substantial portions of real estate loans. If high vacancy rates lead to a wave of delinquencies in commercial loans, these banks may face significant financial challenges. Although larger banks are more diversified and better capitalized, the interconnectedness of the financial system means that regional bank failures could still have ripple effects, potentially straining the wider economy.

What strategies can be employed to mitigate the effects of the commercial real estate crisis?

To mitigate the effects of the commercial real estate crisis, several strategies can be considered. Firstly, reducing long-term interest rates could facilitate refinancing, alleviating some financial pressures on borrowers. Secondly, implementing policies that encourage the conversion of vacant office spaces into affordable housing can help address the dual issues of high vacancy rates and housing shortages. Lastly, restoring consumer confidence and improving overall economic conditions can also bolster demand for commercial properties, aiding recovery.

How might the commercial real estate crisis affect consumers?

The commercial real estate crisis may have various implications for consumers, particularly through potential losses in pension funds tied to commercial property investments. Additionally, if regional banks suffer significant losses, tighter lending practices may ensue, impacting consumers’ access to credit and loans. While some sectors of the economy remain robust, a cascade of failures in commercial real estate could ultimately lead to tighter financial conditions that affect consumer spending and economic stability.

| Key Point | Details |

|---|---|

| Office Vacancy Rates | Vacancy rates in major U.S. cities range from 12% to 23%, down from pre-pandemic levels. |

| Impact of High Vacancy on Real Estate Values | High vacancy rates are depressing property values, leading to potential economic risks. |

| Commercial Mortgage Debt | 20% of the $4.7 trillion in commercial mortgage debt is due this year, potentially affecting banks’ outcomes. |

| Expected Bank Losses | Firms in commercial real estate might see their equity wiped out, impacting bank loan repayments and stability. |

| Differences in Market Conditions | Unlike the U.S., European occupancy rates are more stable, due to smaller homes and shorter commutes. |

| Bank Preparedness | Large banks are likely more resilient due to stricter regulations post-2008; regional banks may face higher risks. |

| Potential Solutions | Refinancing could help, but is unlikely without a significant drop in interest rates or a recession. |

| Broader Economic Effects | Despite losses, consumer impact is limited due to a solid job market and a booming stock market. |

| Dangers of Regional Bank Failures | Failures among smaller banks, if they occur, may not affect larger institutions significantly. |

Summary

The commercial real estate crisis looms as high office vacancy rates and $4.7 trillion in mortgage debt come due, threatening economic stability. Despite fears of widespread bank failures, experts argue that large banks are better equipped to handle potential losses due to stricter regulations implemented post-2008 financial crisis. However, the downturn could lead to significant regional impacts and instability within smaller banks, necessitating close monitoring of the market conditions and potential interventions to prevent a larger economic fallout.